I love everything about social media. From how it keeps us connected to our family and friends to the sharing of GIFs and memes. My obsession with social media started back in college when I became an early adopter of an online application called Facebook. It was clever little tool used by us “pre-Millennials” to find keggers and house parties. Little did I know, I was about to get wrapped up in something far greater than finding free beer (if there is such a thing). As I matured and shifted gears into the real world, social media did too. However, it wasn’t until I applied it to my business that I madly fell in love with it.

Learning to use social media as a marketing tool was (don’t say it) a game changer (he said it). Not only did it help me keep tabs on my my great aunt Yola, but it also rapidly expanded my off and online presence. It allowed me to share relatable first and third-party content to specific audiences, obtain powerful analytics used to further shape my marketing strategy and, most importantly of all, become a thought leader in the profession. It sounds wonderful, but none of it happened over night. While is has been a huge learning experience these last last five years, it’s all been worth it.

Then there are the financial professionals that have chosen a less strategic (and dignified) approach to social media marketing. They are the self-proclaimed “financial advisors” and insurance professionals that lurk inside your local Facebook groups. If you are a member of one of these groups (i.e. moms), you know exactly what I am talking about. If you’re not familiar with them, hang tight as I am going to share some examples based on REAL posts from “real” professionals that I found and have been submitted to me over the past few weeks.

Now, what offends me about these posts isn’t just how outrageously tacky (if not slimy) they are from an advertorial standpoint. No. It’s that they are being posted with a blatant disregard to industry rules and regulations. Rules that are designed to protect consumers from harmful sales practices. At best, these posts are dripping in negligence, which is sad because you would think that a professional would at the very least be aware of their own rules. Unfortunately, each is post is a compliance nightmare, which is exactly why I asked some of the best compliance experts in the profession to weigh in. You’re might want to sit down for this.

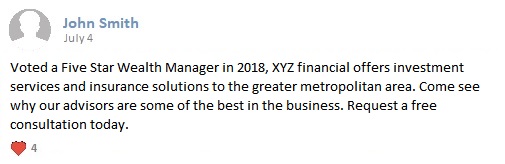

Example #1: Nice trophy.

Compliance’s Take:

Compliance’s Take:

- Appropriate disclosure is required for awards (i.e. number of entrants, methodology).

- How is the claim “best in the business” substantiated? Disclosure would be required.

- How do you get the free consultation? Via DM? Leaving a comment could lead to individuals to publicly giving out their personal contact information. Adding a website link could save this post, but I don’t see that here.

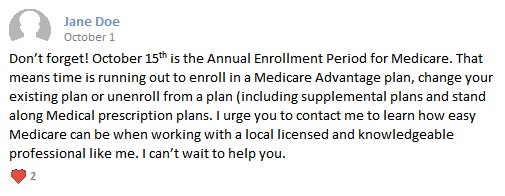

Example #2: Such urgency, much concern!

Compliance’s Take:

Compliance’s Take:

- This creates false sense of urgency without adding that the enrollment period is almost 2 months long, ending in December.

- You don’t necessarily require an agent or any assistance when enrolling in Medicare. Pushing that idea contributes to the sense of urgency. It can be easy if you do it alone too – you just need the time to read and go over all the information.

- As this ad is about Medicare, so the urgency can be viewed as predatory, since it is targeting seniors by default.

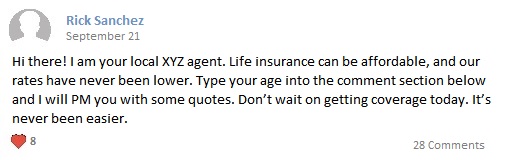

Example #3: F— it! We’re doing it live!

Compliance’s Take:

Compliance’s Take:

- Huge red flag here, asking for people to publicly display their PII (Personally Identifiable Information)/SPI (Sensitive Personal Information).

- Quotes shouldn’t be given over PM, as they can’t be monitored and they are not in writing.

Yikes! If you think this is a problem, you don’t know the half of it. If you’re like me and find these social media marketing tactics disgusting, just wait until I come across a post about how some broker can generate guaranteed returns or, worse yet, just flat out recommends a specific investment.

Sadly, I’m positive it’s already out there as there appears to be no shortage of “bad actors” doing bad things in the financial services industry. These are the folks that make it hard for good professionals to shine, especially when it comes to using tools that can be seriously helpful for growing one’s business. Unfortunately, these posts are everywhere and they go unchecked because regulators and compliance offices don’t even know they exist. Most groups are closed off from the public. You need to be invited in.

I am banging on the same drum that many of my respected colleagues have been banging on for years now. That the financial services industry is struggling to adapt to how quickly the business is changing. Whether it’s the confusion surrounding professional titles, the lack of transparency regarding fee structures or just the overall lack of a fiduciary standard, social media is another example of a dark corner in which shady professionals can hide. While I remain optimistic that the invisible hand will continue to pull these weeds from the proverbial garden, I also put these hopes into action by doing what we can to make the public more informed.

I call it advisor activism. It’s the conscientious decision made by us good guys and good girls to nudge things further along in the right direction. It means that if you see something that’s obviously wrong, you’re not afraid to call it out. And you don’t need to get in anyone’s “face” or make a scene when doing it. In cases such as the one’s I’ve shared here, you can simply contact the group’s administrator(s) to let them know what’s going on and why posts like these are more harmful than helpful. More than likely, the post removed and a warning will be issued to the group member. I bet they’d be too embarrassed or afraid to ever try it again.